The Hill

The AI bubble could be worse than the dot-com bust

Skip to content

The views expressed by contributors are their own and not the view of The Hill

A growing chorus of analysts are beginning to question the sustainability of current market valuations, arguing that a reality check may be overdue.

Concerns about speculative excess have grown amid heightened enthusiasm, and potential risks, surrounding the SpaceX IPO, where an initial offering price of $135 per share valued the Elon Musk-led company at over $1.75 trillion, as well as the forthcoming mega-IPOs of two leading AI firms, Anthropic and OpenAI.

Analyst forecasts indicate that Alphabet, Amazon, Meta Platforms, Microsoft, and Oracle (the so-called hyperscalers) will spend around $755 billion on AI-related capital expenditures in 2026. So far this year, strong earnings growth has provided the impetus for the parabolic spike in some stock prices.

However, extrapolating from recent robust growth in semiconductor and memory chip revenues and expecting sustained long-term outperformance is risky, as it relies on the uncertain assumption that the current boom in AI infrastructure spending will continue unabated. Major hyperscalers are already resorting to additional debt and equity financing to support their elevated capital expenditures, since even their substantial free cash flow is becoming insufficient to fund the escalating investments needed for AI infrastructure.

The current stock market boom and the American economic performance is being fueled by a self-reinforcing cycle. Gains in a handful of AI-focused stocks are enabling major tech firms to invest heavily in the infrastructure that investors expect will drive future growth. This spending boosts GDP both directly, through massive capital investment, and indirectly, through the increased purchasing power of the wealthiest individuals.

But with both the broader economy and the ongoing bull market relying heavily on a concentrated AI-driven boom, the fallout from a burst bubble could be severe.

There is increasing urgency around assessing whether the AI-driven stock market rally of recent years has evolved into a full-fledged equity bubble. Insights from previous technology-fueled bubbles can provide useful perspective and help contextualize current fears regarding the emergence of an AI bubble.

In “Manias, Panics, and Crashes,” economic historian Charles Kindleberger characterized asset bubbles as episodes of speculative mania in which asset prices become disconnected from their underlying fundamentals, fueled by investor psychology and expanding credit, before ultimately collapsing. His insights remain pertinent amid growing evidence of irrational exuberance in the stock market.

Real-world bubbles are rarely built on pure delusion. Financial historians, William Quinn and John Turner, argue that technological innovations can trigger asset bubbles by creating unusually high profits for firms that develop and drive the early adoption of a new technology, resulting in substantial increases in their stock prices. These gains attract momentum-driven investors, while elevated valuations encourage many technology-related firms to enter public markets.

Historical examples include the roaring twenties and the dot-com bubble. Although valuations may seem excessive to seasoned investors, they can persist because the economic implications of a new technology are highly uncertain, making accurate valuation difficult.

At the same time, intense media coverage and investor enthusiasm attract additional participants, often supported by a “new era” narrative that portrays exceptionally high prices as justified. As optimism takes over, traditional valuation rules are ignored. People buy not for intrinsic value or future profits, but in hopes of selling to someone else at an even higher price — the “greater fool.”

In “Bubbles and Crashes,” Brent Goldfarb and David Kirsch examine 58 major technological innovations and identify four conditions associated with bubble formation: high levels of uncertainty surrounding the technology, the participation of novice investors, the availability of investment opportunities in pure-play firms that focus exclusively on the technology and the existence of a compelling narrative about its future potential.

In the current context, while the economic and financial impact of the AI revolution remains uncertain, public excitement has reached extraordinary levels, and exaggerated claims about the technology’s transformative potential are widely circulated.

Retail investors have driven notable gains in AI-related stocks, and their persistent “buy the dip” behavior may have prevented larger market corrections in recent months. Intriguingly, passive investing has expanded to a point where it is influencing market behavior rather than merely reflecting it. In a highly concentrated market, it can channel capital to the biggest winners, amplify momentum, and inflate valuations beyond fundamentals.

If the AI bubble bursts, the economic fallout could be far more damaging than the dot-com crash. The U.S. economy is in a weaker position today, with growth increasingly dependent on high-income consumers, a trend highlighted by a recent New York Fed study. At the same time, substantial AI-related capital expenditures have become an important driver of recent U.S. GDP growth, raising the risk that any sharp pullback in investment could have broader economic repercussions.

Unlike today’s unbalanced economy, the late-1990s expansion was supported by stronger overall economic performance. Real GDP increased by more than 4 percent annually from 1997 to 2000, and the resultant prosperity was widely shared.

Furthermore, in contrast to the 1998 to 2001 period, when the federal government posted budget surpluses for four years in a row, the U.S. has experienced large deficits since 2020.

Federal debt has climbed to more than 120 percent of GDP, compared with 54.5 percent in 2001. Such historically high levels of public debt create significant financial risks. If the benchmark bond yield rises above 5 percent, it could trigger a sharp repricing of risky assets and deflate the AI bubble.

Vivekanand Jayakumar, Ph.D., is an associate professor of economics at the University of Tampa).

Tags

Anthropic

Elon Musk

Elon Musk

OpenAI

SpaceX

Copyright 2026 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.

View original source — The Hill ↗

Related stories

BBC

BusinessJun 5, 2026 · 1 min

Is there an AI stock market bubble, and is it ready to burst?

BBC

MarketWatch

BusinessJun 8, 2026 · 1 min

What nine different indicators say about market exuberance, according to Goldman Sachs

MarketWatch

MarketWatch

BusinessJun 5, 2026 · 1 min

The stock market is at its frothiest since the global financial crisis, proclaims Citi. Why dip buyers shouldn’t bail…

MarketWatch

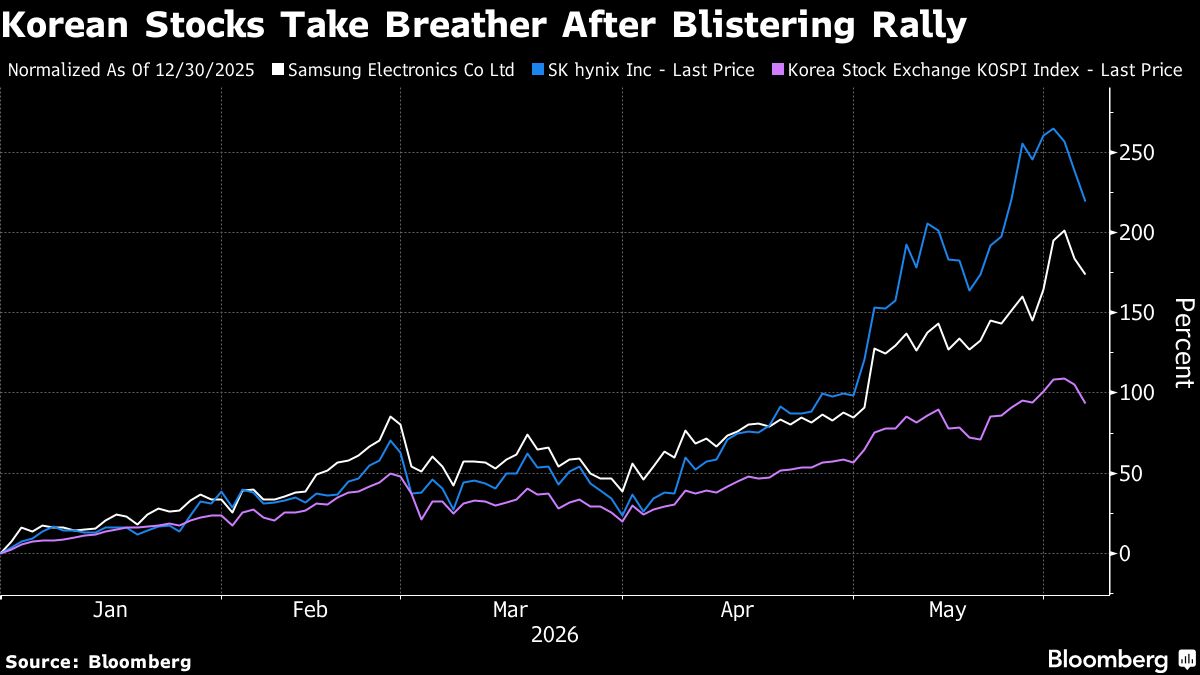

Bloomberg

BusinessJun 7, 2026 · 1 min

World’s Hottest Market Korea Has Bulls Reaching for Protection

Bloomberg