Rio Times

Brazil’s MRV Sells US Apartments at a Loss to Cut Its Debt

Markets · Brazil · Real Estate

— Key Facts

—The deal. Brazil’s biggest homebuilder, MRV, sold two Texas apartment complexes, Ten Oaks and Rayzor Ranch, for $139m (R$716m) through its United States arm, Resia.

—Sold cheap. The pair were on the books at $188m, so the sale crystallises a 26% loss to book value, accepted to bring cash in sooner.

—Debt cut. The transaction lowers MRV’s group net debt by $87m, a drop of about 7.5%, with completion due in July.

—Halfway out. Sales since the December 2024 plan now total $380m, close to half the $800m of US assets MRV aims to shed by the end of 2026.

—The culprit. High United States interest rates and a glut of new apartments in cities such as Dallas and Houston held down rents and slowed the buildings’ leasing.

—Market view. Analysts at BTG keep a buy rating with a R$12 target, against a recent price near R$7.58, betting the cleanup unlocks value.

The latest MRV Texas sale is a study in choosing certainty over price: the company took a clear markdown on two apartment complexes simply to get the cash and the debt off its books faster.

Brazil’s largest affordable-housing builder is unwinding its American adventure, and it is willing to take a haircut to do it. MRV has agreed to sell two Texas apartment complexes for a price well below what they are valued at.

The buildings, called Ten Oaks and Rayzor Ranch, went for $139m, around R$716m, according to the company’s filing. They sit on the company’s books at $188m, so the deal locks in a loss of roughly a quarter of their stated worth.

MRV runs its United States business through a subsidiary called Resia, which builds large rental apartment blocks owned by a single landlord. That arm has become a drag on the parent, and the priority now is cash, not growth.

Why the MRV Texas sale was struck below value

The discount was not uniform. Ten Oaks was the weaker asset, valued at $122m but sold for $86m, a 30% cut, with only 73% of its flats occupied.

Rayzor Ranch held up better, fuller at 93% occupancy and sold at about a 20% discount. Neither building had yet reached the steady income level that would command full price.

The cause is the American rate cycle. Borrowing costs in the United States have stayed high for longer than MRV expected, while a wave of new apartments in Dallas, Houston and Atlanta pushed rents down and slowed leasing.

In that setting, waiting is expensive. Rather than hold the buildings for a better day, MRV chose to sell now and use the proceeds to shrink debt, judging the relief worth the markdown.

Halfway through the retreat

The sale is a milestone in a plan announced in December 2024 to raise $800m by shedding American land and buildings. With this deal, MRV has now sold about $380m worth, close to half the target.

It also marks a clear pickup in pace. The company had managed roughly $241m of sales by the end of the first quarter, so the recent stretch has moved faster than the slow start that frustrated investors.

What is left tells its own story. Only one older building, Memorial, valued at $109m, remains in the legacy pile, while two newer projects, Golden Glades and North City, are expected to be sold at a profit.

In other words, MRV is clearing the hard, loss-making assets first and keeping the profitable ones for later. The shape of the exit is improving even as the early sales sting.

There is a second benefit beyond the headline figure. The deal also trims about $46m of minority interests, tidying the ownership structure as well as the debt load.

The controlling Menin family has gone further, saying it may eventually separate Resia from the group entirely. Options floated range from a spin-off to bringing in an outside partner once the debt is under control.

Why it matters for investors

For a foreign reader, the appeal of MRV was always its home market, where Brazil’s vast housing shortage and a large government subsidy programme support steady demand. The United States was the complication.

Cutting the American exposure is meant to simplify the company and make its earnings easier to read. Analysts at BTG keep a buy rating and a R$12 target, against a recent price near R$7.58, on the view that a cleaner MRV is worth more.

The shares have spent the past year near multi-decade lows, so the market wants proof, not promises. Each completed sale, even at a loss, is a step toward the simpler, less indebted company management has promised.

Frequently Asked Questions

What did the MRV Texas sale involve?

MRV agreed to sell two Texas apartment complexes, Ten Oaks and Rayzor Ranch, for $139m through its United States arm Resia. The price was about a quarter below their book value, and the deal cuts group net debt by $87m.

Why did MRV sell the buildings at a loss?

High United States interest rates and an oversupply of apartments held down rents and occupancy, so the buildings were not yet earning full value. MRV chose to take the markdown to bring in cash and reduce debt sooner.

How far along is MRV’s United States exit?

Since the December 2024 plan, MRV has sold about $380m of American assets, close to half its $800m target for the end of 2026. It is clearing loss-making assets first and keeping profitable projects for later.

In depth

Brazil inflation, Selic and rates 2026

Buying property in Brazil (foreigner guide)

The Rio Times · Power Map

See who really holds power in Latin America

Click to open the Power Map →

View original source — Rio Times ↗

Related stories

Bloomberg

BusinessJun 23, 2026 · 1 min

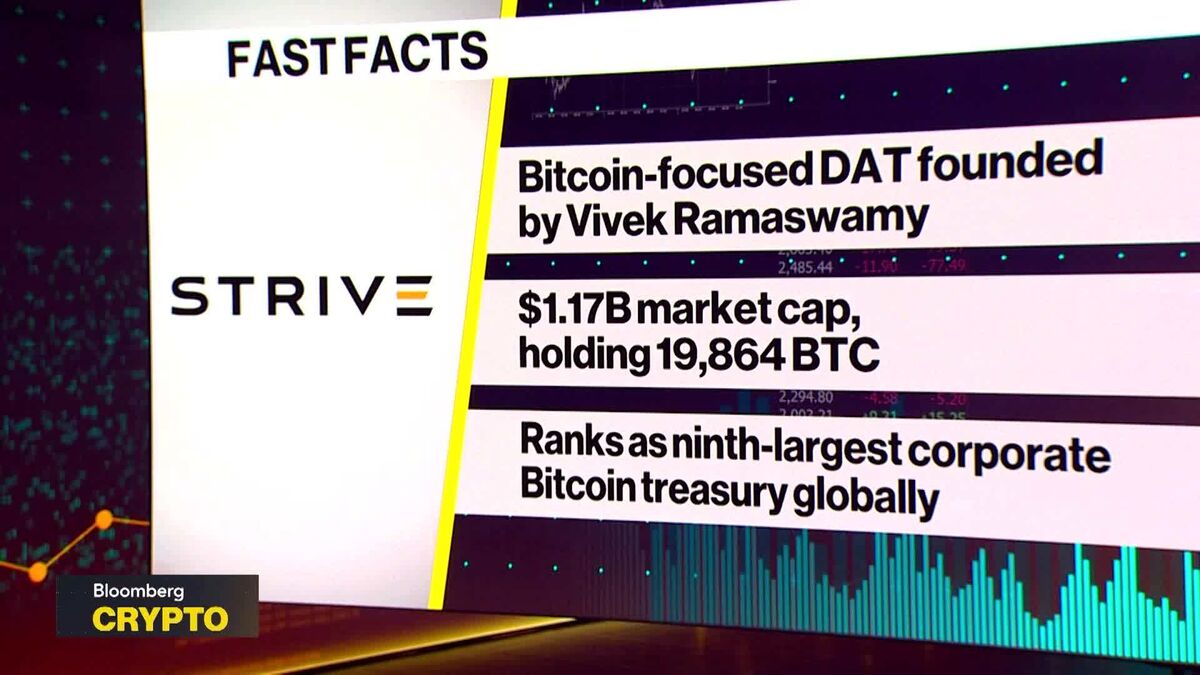

Strive Is Buying Bitcoin Hand-Over-Fist, CEO Says

Bloomberg

CNBC

BusinessJun 23, 2026 · 1 min

SpaceX raises $25 billion in debt sale less than two weeks after IPO

CNBC

Bloomberg

BusinessJun 23, 2026 · 1 min

Argentine Economy Grew More Than Expected in First Quarter

Bloomberg

Financial Times

BusinessJun 23, 2026 · 1 min

Alibaba sues Pentagon over inclusion on Chinese military blacklist

Financial Times