Indian Express

New EPF Scheme, 2026: What changes for provident fund subscribers

The Ministry of Labour and Employment’s move is part of the implementation of the Code on Social Security, 2020, with the new scheme coming into effect from June 29.

The recent decisions taken by the retirement fund body, the Employees’ Provident Fund Organisation (EPFO), regarding partial withdrawals and streamlining of withdrawal categories have been incorporated into the new scheme, along with an explicit mention about mandatory and voluntary contributions above the statutory wage ceiling.

For contract workers, the concept of ‘principal employer’ has been introduced in the scheme for the first time. This is in line with the provisions of the labour codes.

The EPF Scheme, 2026 states that the employer will be required to pay both the employer’s contribution and the employee’s contribution, in the first instance, along with administrative charges or other fees for an employee directly employed by the employer or through a contractor (not registered independently), within 15 days of the close of every month.

In cases where the PF payment is made by the contractor, the ultimate responsibility for contributions will be with the principal employer.

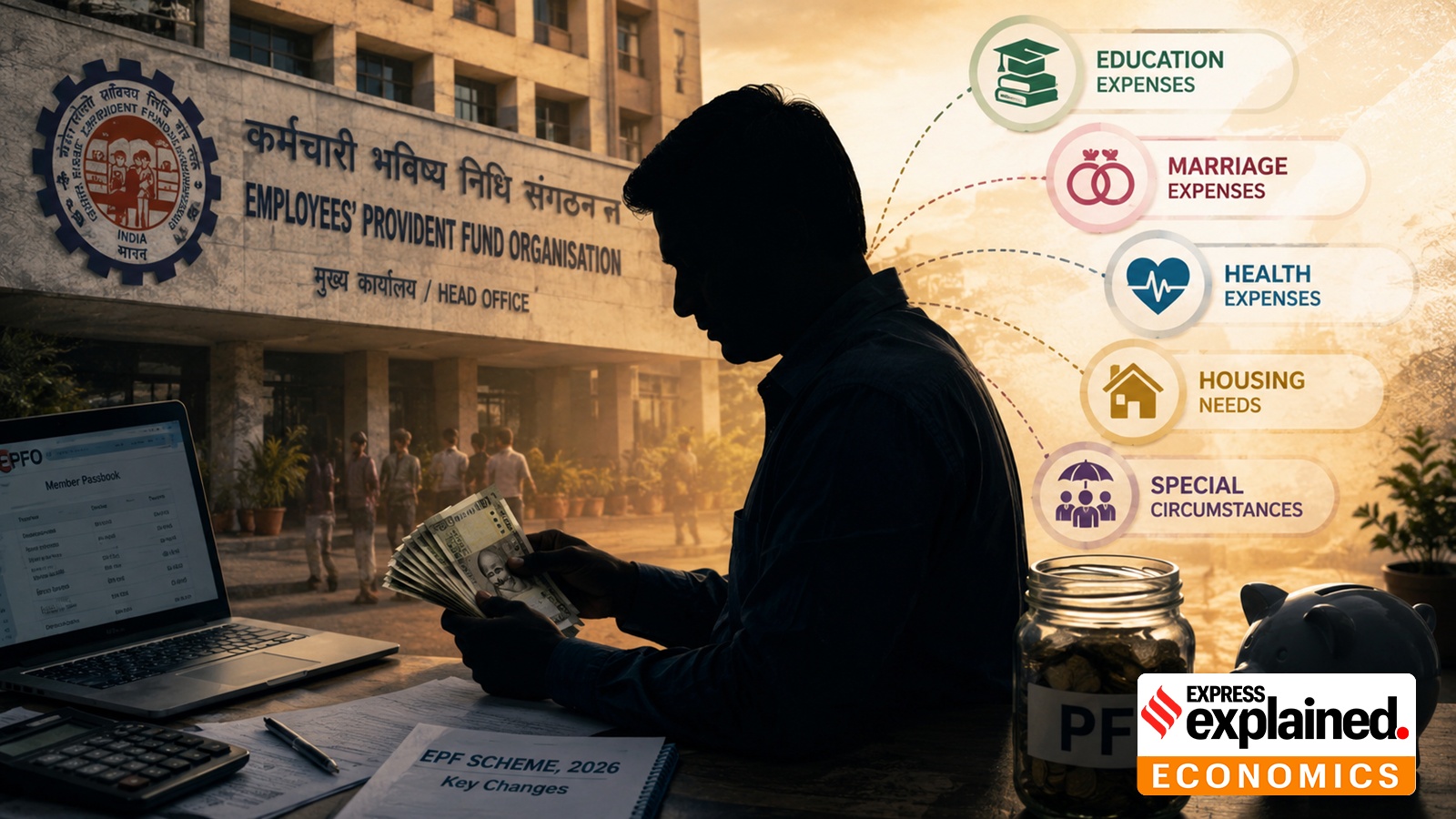

What has changed in the EPF Scheme, 2026?

In October 2025, the EPFO announced a slew of changes to its withdrawal norms by streamlining the withdrawal categories from 13 to three — essential needs (illness, education, marriage); housing needs; and special circumstances, along with an introduction of a minimum balance of 25%.

Story continues below this ad

The new EPF Scheme, 2026 incorporates those changes by allowing members to withdraw funds in case of illness of self and family members, up to 100% of the eligible member balance, after completion of 12 months of total membership of the Fund.

The 100% eligible member balance means withdrawal of 75% of the total funds as 25% is mandatory minimum balance requirement. The full 100% amount can be withdrawn after remaining unemployed for one year.

Members can also withdraw money for the education of self and family members after 12 months’ total membership of the Fund. Partial withdrawal cannot exceed 10 times during the membership. For the marriage of self and family members, an amount up to 100% of the eligible member balance can be withdrawn, and partial withdrawal cannot exceed 5 times during the membership of the Fund.

For housing-related requirements, a member may be allowed partial withdrawal for the purchase of a flat, house; site for construction of a house; construction of a house; repayment of a home loan obtained for purchase, construction of a flat or house or for acquisition of a site; and additions, alterations, renovations or improvements to an existing house or flat. The condition is that such withdrawals will be limited to 75% of total funds after completion of 12 months of total membership in the Fund and partial withdrawal not exceeding five times.

Story continues below this ad

“Members will be able to make partial withdrawals under simplified rules for essential needs such as illness, education and marriage, as well as for housing requirements and other specified special circumstances, subject to prescribed conditions and maintenance of a minimum balance of 25% of aggregate of total contributions to the Fund,” Puneet Gupta, Partner, People Advisory Services, EY India said.

What remains the same in the EPF Scheme, 2026?

The rate of contribution remains the same from the previous scheme at 12% and 10% for certain notified establishments. As per the existing scheme, the rate of contribution is mandatory till the wage ceiling.

The EPF Scheme, 2026 requires provident fund contributions at 12% of wages from both the employer and employee and specifically provides that where wages exceed the statutory wage ceiling, mandatory contributions will be restricted on the wage ceiling amount. Gupta said. “Employees may, however, opt to make voluntary contributions either on wages exceeding the statutory wage ceiling or at a rate higher than the prescribed 12%. Employers also have the option to make matching contributions against such voluntary contributions,” he added.

The new scheme now explicitly states that employees may voluntarily contribute on wages exceeding the ceiling or contribute at a rate higher than 12%, with employers having the option to make matching contributions. “Employees may voluntarily contribute on wages exceeding the ceiling or contribute at a rate higher than 12%, with employers having the option to make matching contributions. Such voluntary contributions may also be reduced or discontinued later by both parties. This is as before, no change. Nothing has been made mandatory afresh in the new scheme,” an official said.

Story continues below this ad

The explicit provision allowing employees or employers to reduce or discontinue such additional voluntary contributions at any time will provide greater flexibility in structuring retirement savings. It will also help people to increase their take-home pay. The employer is liable to pay additional administrative charges on such wages, on which voluntary contributions are paid.

The EPF Scheme, 2026 retains the concept of mandatory coverage for international workers employed in covered establishments. It also clarifies that existing international workers who were members under the EPF Scheme, 1952 will continue as members under the EPF Scheme, 2026. Special provisions for withdrawals for international workers continue, with withdrawals generally permitted only on retirement from service after attaining 58 years of age, except when covered under social security agreements.

View original source — Indian Express ↗

Related stories

TechRadar

TechnologyJul 2, 2026 · 1 min

The 'gorgeous' Microsoft Surface Laptop is the perfect productivity machine for work and study

TechRadar

South China Morning Post

TechnologyJul 2, 2026 · 1 min

Could China’s containerised aircraft launcher reshape rules of modern warfare?

South China Morning Post

TechRadar

TechnologyJul 2, 2026 · 1 min

New report claims AI is leading to job layoffs — but higher-level more educated workers are being hit hardest

TechRadar

ZDNet

TechnologyJul 2, 2026 · 1 min

Plug-in solar poses 6 safety risks, say electrical industry groups - here's when to call a pro

ZDNet