Rio Times

Santander’s Brazil Unit Falls So Far Behind, a Buyout Is in Play

Daily Brief

The morning intel from across Latin America. Free.

By subscribing you agree to our privacy policy. We never share your email.

Markets

Key Facts

—The slump. Santander Brasil units (SANB11) have fallen about 21% in 2026, the worst run among Brazil’s largest banks.

—The split. Meanwhile the Spanish parent’s shares are up roughly 24%, making it continental Europe’s most valuable bank.

—The record gap. The valuation gulf between the two is the widest since the Brazil unit’s 2009 listing.

—The speculation. A UBS analyst says a buyout of the local arm by the parent cannot be ruled out.

—The cause. Rising bad loans, weak lending and low-cost fintech rivals have squeezed the bank in its biggest market.

The gap between Santander Brazil and its Spanish parent has grown so wide that analysts are openly asking whether Madrid will simply buy out the local arm and take it private. The two halves of the same bank are moving in opposite directions.

One side is thriving, the other is stumbling. The result is a rare split that turns an ordinary earnings slump into a live question about corporate structure.

Why Santander Brazil has fallen behind

The share moves tell the story. The Brazil-listed units, known as SANB11, have dropped about twenty-one percent this year, the weakest showing among the country’s biggest banks.

The parent in Madrid has gone the other way. Its stock is up roughly twenty-four percent, and the group has become the most valuable bank in continental Europe, with profits at record highs.

The problem is the Brazilian economy. The local unit leans more heavily on consumer credit than its domestic rivals, which makes its results especially sensitive to the country’s high interest rates and stubborn inflation.

Bad loans are the sore point. The bank’s ninety-day default rate climbed from two and eight-tenths percent to three and three-tenths percent over the year to March, with the strain heaviest among lower-income households and small firms.

Low-cost digital banks add to the pressure. Fintech rivals such as Nubank have pulled customers away from traditional lenders, forcing incumbents to spend more on technology just to hold their ground.

The numbers behind the mood are stark. Recurring profit slipped to about three and eight-tenths billion reais in the first quarter, and return on equity fell to roughly sixteen percent, well below the twenty percent-plus the bank once delivered.

Rivals show what good looks like. Market leader Itaú earns a return on equity near twenty-four percent, a gap that helps explain why investors have punished the Santander unit while rewarding its peers.

Could the parent take Santander Brazil private?

This is where the story turns interesting for investors. The measure that matters is how much the market pays for each unit relative to its book value, and on that basis the Brazil arm now trades at a record discount to its parent.

The gap has widened steadily since early last year, when the first fresh rumors of a possible buyout began to circulate. A cheap subsidiary and a soaring parent are exactly the conditions that invite such a move.

Analysts have started to say so out loud. Thiago Batista of UBS BB Investment Bank said that, looking at the valuation gap and what has happened in the past, he would not rule out a public offer for the shares.

For minority holders, that prospect cuts both ways. A buyout could deliver a quick premium on a beaten-down stock, but it would also remove one of the few large international banks listed on the São Paulo exchange.

For now, the shares still pay well while investors wait. The units carry a dividend yield near eight and a half percent, and the local arm is valued at about one hundred and twenty billion reais, or roughly twenty-three billion dollars.

The wider lesson is about divergence inside a single company. When a subsidiary and its parent drift this far apart, the market starts to price the possibility that the structure itself will change.

Frequently Asked Questions

Why has Santander Brazil stock fallen in 2026?

Santander Brazil units are down about twenty-one percent this year, hurt by rising bad loans, weak credit growth and pressure from low-cost digital banks. Its heavier exposure to consumer lending makes it especially sensitive to Brazil’s high interest rates and inflation.

Could the parent take Santander Brazil private?

A UBS BB analyst says a buyout cannot be ruled out, because the Brazil unit now trades at a record discount to its Spanish parent. A cheap subsidiary and a soaring parent are the classic conditions for a take-private offer, though nothing has been announced.

The Rio Times · Power Map

See who really holds power in Latin America

Click to open the Power Map →

View original source — Rio Times ↗

Related stories

The New York Times

BusinessJul 7, 2026 · 1 min

Is ‘The View’ a News Show? ABC Says That’s Already Settled.

The New York Times

CNBC

BusinessJul 7, 2026 · 1 min

Strait of Hormuz threat level raised to 'severe' after Iran attacks tankers using U.S. Navy route

CNBC

Bloomberg

BusinessJul 7, 2026 · 1 min

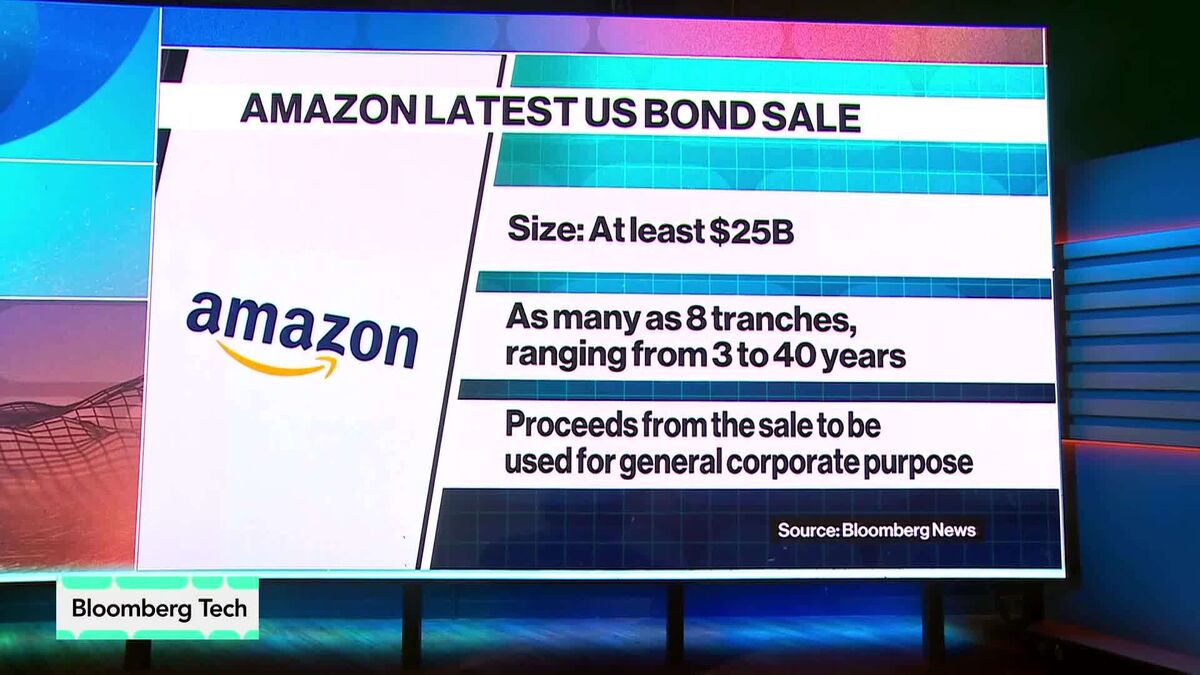

Amazon Fuels AI Debt Boom With Another Bond Sale

Bloomberg

Philippine Daily Inquirer

BusinessJul 7, 2026 · 1 min

BSP warns of sanctions vs banks, e-wallets that fail to lower transfer fees

Philippine Daily Inquirer